Six things your competition is probably already thinking about

Introduction

The conversation in healthcare today is no longer about whether competition is good or bad. It’s about who’s eating your lunch and what to do about it.

As more and more countries adopt market-based approaches for healthcare delivery, executive attention will continue to shift from the merits of competition to strategies for staying alive and prospering. Increasing pressures for improved clinical, operational, and financial performance leave little time for trial and error.

Researchers have identified 6 key areas that pay the most dividends in terms of a medical institution’s ability to survive and position itself for growth. This White Paper presents the findings from that research and explores strategies for strengthening competitiveness in each key area.

Don’t think competition is just about not getting eaten. It’s also about competing for huge prizes; with approximately 12 million cross-border patients worldwide, for example, the global market for medical tourism alone is estimated to be worth tens of trillions of dollars.1

How ready are you to compete?

Aging populations and

cuts in public healthcare funding are driving new levels of competitive

pressure

Current economic pressures on healthcare systems and institutions are already straining the resources and ingenuity of healthcare decision makers.

As global populations continue to age and governments continue to cut back on public healthcare funding, the ability to strengthen clinical capabilities, patient outcomes, and process efficiency is rapidly becoming the battleground on which competitive strategies are being fought.

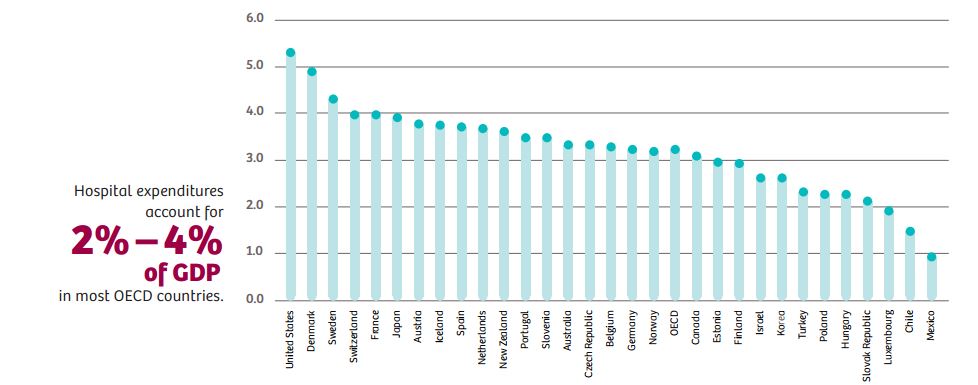

Nowhere is this more true than in hospitals, whose expenditures worldwide represent the single largest component of health spending, an average of 30% among OECD countries.2

Many countries have adopted market-based approaches in recent years to intensify competition, especially in publicly controlled hospital sectors. In Norway, patients are free to choose between public hospitals across the country.3

In Denmark, patients are allowed to seek treatment free of charge at a private-sector hospital or hospitals abroad if the waiting time for a given treatment exceeds two months in the public health system. Public hospitals there have risen to the competitive challenge: waiting times have fallen by 33% in most parts of the Danish public system since the introduction of competitive reforms in 2002.4 As health systems continue to shift the primary locus of patient care from hospitals to less costly non-hospital settings, pressures on hospitals can be expected to grow even stronger.

Lessons from the largest, most competitive market in the world The United States not only has the largest healthcare expenditures in the world (16.4% of GDP), but other than Chile, it is the only OECD country where public spending accounts for less than 50% of total health spending. The OECD average is 73%.5

What can be learned from the United States’ decades-long primarily free-market experience?

Six ways to survive – and even grow –in a competitive world

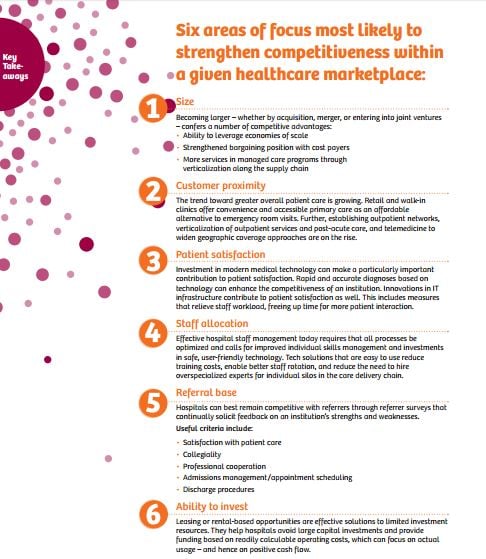

1. Size counts

Becoming larger – whether by acquisition, merger, or entering into joint ventures –confers a number of competitive advantages:6

• Ability to leverage economies of scale

• Strengthened bargaining position with cost payers

• More services in managed care programs through verticalization along the supply chain

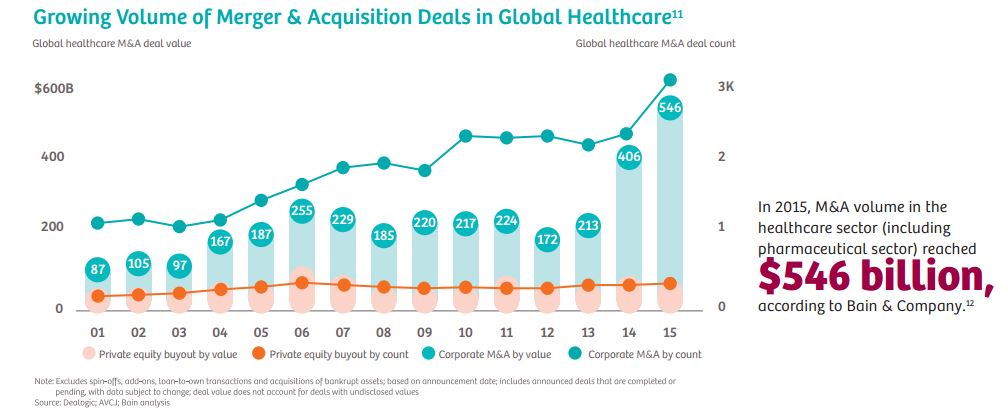

It’s little wonder that mergers and acquisitions in the healthcare sector are growing every year.7

Both horizontal and vertical consolidation are up significantly. From 2010 to 2014, 457 hospital merger and acquisition deals were announced, involving close to 1,000 hospitals.8

Population health management favors larger providers able to

offer a comprehensive range of services. According to King’s Daughters Health

System – a non-profit health system covering six counties in Kentucky and Ohio

– Vice President and Chief Strategy Officer Matt Ebaugh,

“If you’re not able to provide full service, including sub–specialties, it will be very difficult to go after a full at–risk contract. When health insurance companies are looking at your ability to deliver care for a patient population and you don’t have certain services, that would be a problem. It is about scale now.”9

Surveys show that U.S. hospital managers see the verticalization of outpatient services and post–acute care as a way to improve patient outcomes and increase market share and revenues.10 The most common objectives of healthcare partnerships in the United States are increased market share, improved operational cost efficiencies, improved financial stability, expanded geographical coverage, and greater strength in payer negotiations.

2. It pays to be where the patients are

2. It pays to be where the patients are

The U.S. healthcare market is moving quickly toward greater overall outpatient care. From 2003 to 2012, Medicare spending on outpatient hospital services in the United States increased by 136.5% – significantly outstripping inpatient services.13 Retail and walk-in clinics offer convenience and accessible primary care as an affordable alternative to emergency room visits. CVS already operates more than 1,000 retail clinics and plans to have 1,500 in 35 states by 2017. Demographic targets call for half of all Americans to have a CVS MinuteClinic within 10 miles of home.14

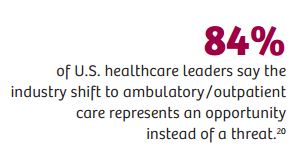

Following their success in the primary care market, retail clinics are now looking to expand further into chronic and specialized care. Rather than see this as a reason for worry, far-looking hospital managers see an opportunity. Many providers, for example, have already entered into partnership agreements with players such as CVS and Walmart. For hospitals, such partnerships can lead to advantages via access to a much broader database for targeted population health management programs. When hospital admission is required for more serious illness, the fact that the hospital’s own doctors have already built patient contacts among the retail clinic’s customer base provides a competitive advantage.

The establishment and development of outpatient networks is particularly attractive for healthcare providers. “Whether you’re in population health or whether you’re in fee-for-service, it makes sense to try to create a broader network that can reach more people and have your organization achieve significant outcomes in less capital-intensive ways than by just building hospitals, which are among the most risked investment strategies,” according to Scott Nordlund, executive vice president for growth, strategy, and innovation at Trinity Health, a Livonia, Michigan-based nonprofit with facilities in 21 states.15

Surveys show that U.S. hospital managers see the verticalization of outpatient services and post-acute care as a way to improve patient outcomes and increase market share and revenues.16 In the United States, for example, approximately 40% of all Medicare acute care patients are discharged to a post-acute care setting – an attractive market in which hospitals can participate through verticalization.17 A close integration with post-acute facilities also offers hospitals the advantage of being able to discharge patients sooner, freeing beds for more patients.18

Telemedicine is proving to be a great leveler of geographic advantage as well. Here, interestingly, it’s instructive to look to emerging healthcare markets. The Diagnostic Treatment Centre at the International Institute of Biological Systems (DTC IIBS) in St. Petersburg, Russia – the first privately owned MRI center in the country – performs about 1.2 million MRI scans per year at 77 centers. All centers are merged into a single telemedical network. The most experienced doctors supervise their colleagues in other cities from the consulting center in St. Petersburg.19

3. Leave the customer satisfied

In the U.S., since 2012, a growing portion of hospital reimbursements has been tied to Hospital Consumer Assessment of Healthcare Providers and Systems (HCAHPS) scores. HCAHPS performance will determine up to 2% of all Medicare payments for hospitals and health systems by 2017.21 The tendency is that this amount will increase in the future.

“The financial risk for not giving patients a good experience now becomes very high,”says Lori Kondas, senior director for the Office of Patient Experience at the Cleveland Clinic in the United States. “Hospitals or practices that don’t stand behind the fact that we need to take care of our patients both behaviorally and clinically stand to lose a significant amount of money”.22

The financial implications of patient experience can be seen most clearly in the fact that 40% of U.S. healthcare leaders say their organizations now have a C-level executive on the senior leadership team in charge of promoting and coordinating patient experience across departments within their organization. An additional 10% plan to add such a position within the next three years.23

Investment in modern medical technology can make a particularly important contribution to patient satisfaction. Rapid and accurate diagnoses based on technology can enhance the competitiveness of an institution.24 Innovations in IT infrastructure contribute to patient satisfaction as well. This includes measures that relieve staff workload, freeing up time for more patient interaction.

While patient satisfaction is a clear marker for competitiveness, it’s important to weigh the need to keep patients happy against the need to keep them healthy and the need of institutions to remain financially sound. A team of UC Davis researchers has found, for example, that people who are the most satisfied with their doctors are more likely to be hospitalized, accumulate more healthcare and drug expenditures, and have higher death rates than patients who are less satisfied with their care.25

Prior studies have shown that patient satisfaction strongly correlates with the extent to which physicians fulfill patient expectations. Hospitals and providers able to balance responsible healthcare with a commitment to technology and procedures designed to make it easier, faster, and more precise will have a definitive leg up in terms of the overall patient experience.

The May 2013 Harvard Business Review’s article “Health Care’s Service Fanatics: How the Cleveland Clinic leaped to the Top of Patient-Satisfaction Surveys” is a good case study with important insights about how Cleveland Clinic was able to transform itself from a patient experience perspective.26

“Not surprisingly,” says the AMA Journal of Ethics, “It started with CEO Toby Cosgrove, MD, making it a strategic priority, but it ultimately involved a culture change throughout all levels of the organization. As illustrated by the experience of Cleveland Clinic and other healthcare organizations, patient satisfaction can be dramatically improved if one looks beyond the myths and misperceptions to the reality of what can and should be done to enhance the patient experience.”27

4.Smart personnel management is a smart move

Nearly 70% of health workers worldwide are concentrated in Europe and North America.28 Still, even in industrialized countries, skilled healthcare professionals are hard to find. About a third of German hospitals, for example, have problems filling nursing vacancies. According to the Association of American Medical Colleges, the United States will be 90,000 doctors short by 2025.29

Not surprisingly, tech solutions are already proving their value. Effective hospital staff management today requires that all processes be optimized and calls for improved individual skills management and investments in safe, user-friendly technology. Tech solutions that are easy to use reduce training costs, enable better staff rotation, and reduce the need to hire overspecialized experts for individual silos in the care delivery chain.

More flexibility in staff allocation also increases employee satisfaction while freeing doctors and nurses from patient-distant management tasks.30

5. Cultivate

referrals

Practicing active referral management is crucial for a hospital’s ability to influence patient flow. Referring physicians should be viewed and treated as valuable partners.

Referrers may be

broken down into categories:

• Frequent referrers

• First-time referrers

• Local referrers

• Referrers from further afield

• Referrers with high or low revenue potential

• Discipline-specific referrers

The most successful hospitals attempt to cultivate an ongoing relationship with all referring physicians in the catchment areas. Hospitals can best remain competitive with referrers through referrer surveys that continually solicit feedback on an institution’s strengths and weaknesses.

Referrers should be

broken down into categories:

• Satisfaction with patient care

• Collegiality

• Professional cooperation

• Admissions management/appointment scheduling

• Discharge procedures

6. Invest in success

Without adequate profit margins to generate surplus for investment purposes, hospitals enter a dangerous downward spiral: necessary investments fail to occur, which decreases competitiveness, which in turn decreases surplus, preventing investment.

Investing in modern IT, staff training, high-performance equipment, modern premises, and even contemporary room amenities is the price of entry for competing in most markets. However, faced with insufficient public investment financing, hospitals are left to cover such investments themselves.

Leasing or rental-based opportunities are effective solutions to limited investment resources. They help hospitals avoid large capital investments and provide funding based on readily calculable operating costs, which can focus on actual usage—and hence on positive cash flow. According to a Siemens Financial Services survey, more than half of chief financial officers at health organizations worldwide rely on a variety of financing options.31

Overall, healthcare institutions are using smart finance to improve planning, acquire state-of-the art technology, and manage cost-per-outcome in order to offer high-quality care and service to patients, which in turn enhances the organization’s reputation, attracts more patients and staff, deploys clinical services more efficiently and effectively, adapts seamlessly to market changes,and ensures regulatory compliance.

Increasingly, healthcare finance managers are looking to specialist financiers whose in-depth knowledge of medical technology, the healthcare market, and best practice in technology implementation allow them to offer flexible financing arrangements that meet their individual needs.

References

1. Patients Beyond Borders: Medical Tourism Statistics & Facts [Internet]. Raleigh (NC) updated 2016 May 7; cited 2016 June. Available from: www.patients.beyondborders.com/medical-tourism-statistics-facts

2. OECD: Competition in Hospital Services,” OECD Policy Roundtables

3. OECD: Competition in Hospital Services,” OECD Policy Roundtables

4. Dash, P. and Meredith, D.: When and How Provider Competition Can Improve Health Care Delivery [Internet] McKinsey & Company; 2010 November; cited 2016 June. Available from: http://www.mckinsey.com/industries/healthcare-systems-and-services/our-insights/when-and-how-providercompetition-can-improve-health-care-delivery

5. OECD: Country Note: How Does Health Spending in the United States Compare [Internet]; 2015 July 7. Cited 2016 June. Available from: www.oecd.org/unitedstates/Country-Note-UNITED%STATES-OECD-Health Statistics-2015.

6. HealthLeaders Media: Another Study Links Hospital Mergers and Acquisitions to Higher Prices [Internet] 2016 March 28, cited 2016 June. Available from:www.healthleadersmedica.com/finance/another-study-links-hospital-mergershigher-prices.

Full text of study available at: http://www.kellogg.northwestern.edu/docs/faculty/dafny/price-effects-of-cross-market-hospital-mergers.pdf

7. Bain & Company: Global Healthcare Corporate M&A Report 2016 [Internet] Cited 2016 June. Available from: www.bain.de/Images/BAIN_REPORT_HEALTHCARE_MA.pdf

8. American Hospital Association: Trendwatch Chartbook: Chart 2.9: Announced Hospital Mergers and Acquisitions 1998-2014

9. HealthLeaders Media: Industry Survey: Ready, Set, When? The Drawn-Out-Shift to Value [Internet] 2016 January; cited 2016 June. Available from: www.healthleadersmedia.com/report/intel/industry-survey-ready-set-whendrawn-out-shift-value

10. Bees, J: Intelligence Report: The Outpatient Opportunity-Expanding Access, Relationships and Revenue [Internet] 2016 January 7; cited 2016 June. Available from: http://www.healthleadersmedia.com/quality/intelligence-report-outpatientopportunityexpanding-access-relationships-and-revenue

11. Bain & Company: Global Healthcare Corporate M&A Report 2016 [Internet] Cited 2016 June. Available from: www.bain.de/Images/BAIN_REPORT_HEALTHCARE_MA.pdf

12. Bain & Company: Global Healthcare Corporate M&A Report 2016 [Internet] Cited 2016 June. Available from:www.bain.de/Images/BAIN_REPORT_HEALTHCARE_MA.pdf

13. Medicare Payment Advisory Commission: Healthcare Spending and the Medicare Program [Internet] 2014 June; cited 2016 June. Available from: www.medpac.gov/documents/piublicagtions/june14databookentirereport.pdf

14. Sussman, A.: What’s Next for MinuteClinic; CVS Health [Internet]; cited 2016 June. Available from: www.cvshealth.com/thought-leadership/expertvoices/whats-next-for-minute-clinic

15. Bees, J: Intelligence Report: The Outpatient Opportunity-Expanding Access, Relationships and Revenue [Internet] 2016 January 7; cited 2016 June. Available from: http://www.healthleadersmedia.com/quality/intelligencereport-outpatient-opportunityexpanding-access-relationships-and-revenue-?Page=0%2C4

16. Bees, J: Intelligence Report: The Outpatient Opportunity-Expanding Access, Relationships and Revenue [Internet] 2016 January 7; cited 2016 June.Available from: http://www.healthleadersmedia.com/quality/intelligencereport-outpatient-opportunityexpanding-access-relationships-and-revenue-?Page=0%2C4

17. Deloitte: Going Vertical: Opportunities for Hospitals to Embrace Post-Acute Care, [Internet] 2014, cited 2016 June. Available from: www.2deloitte.com/content/dam/Deloitte/us/Documents/life-sciences-healthcare/us-Ishc-goingvertical.pdf

18. Bees, J: Intelligence Report: The Outpatient Opportunity-Expanding Access, Relationships and Revenue [Internet] 2016 January 7; cited 2016 June. Available from: http://www.healthleadersmedia.com/quality/intelligencereport-outpatient-opportunityexpanding-access-relationships-and-revenue-?Page=0%2C4

19. Diagnostic Treatment Centre of Biological Systems (Internet); cited 2016 June. Available from: www.idc.ru/en

20. Bees, J: Intelligence Report: The Outpatient Opportunity-Expanding Access, Relationships and Revenue [Internet] 2016 January 7; cited 2016 June. Available from: http://www.healthleadersmedia.com/quality/intelligencereport-outpatient-opportunityexpanding-access-relationships-and-revenue-?Page=0%2C4

21. Betbeze, P, HCAPS: Making a Difference While there is Still Time (Internet);HealthLeaders Media 2016 November 11; cited 2016 June. Available from:www.healthleadersmedia.com/marketing/hcahps-making-difference-whiletheres-still-time

22. Beaulieu, D., AMGA 2016: Linking Patient Experience to the Bottom Line [Internet] 2016 March 17; cited 2016 June. Available from:www.healthleadersmedia.com/physician-leaders/amga-2016-linking-patientexperience-bottom-line?page=0%2C1

23. HealthLeaders Media: Patient Experience: Cultural Transformation to Move Beyond HCAHPS [Internet]; 2015 October; cited 2016 June. Available from: www.healthleadersmedia.com/report/intel/patient-experienceculturaltransformation-move-beyond-hcahps

24. The Beryl Institute, Patient Experience Journal (Internet); cited 2016 June; Available from: www.pxjournal.org

25. UC Davis Health System: Patient Satisfaction Linked to Higher Health-care expenses and mortality” (Internet); 2012 February 13; cited 2016 June. Available from: www.ucdmc.ucdavis.edu/publish/news/newsroom 6223

26. Merlino, JI, Raman, A. Health Care’s Service Fanatics [Internet] Harvard Business Review, 2013 May; cited 2016 June. Available from: www.hbr.org/2013/05/health-cares-service-fanatics

27. Siegrist, RB Jr., Patient Satisfaction: History, Myths, and Misperceptions (Internet); AMA Journal of Ethics, 2013 November; cited 2016 June. Available from: www.journalofethics.ama-assn.org

28. World Health Organization: The World Health Report 2006: Health Workers (Internet); cited 2016 June. Available from: www.who.int/whr/2006/06_chap1_en.pdf

29. Association of American Medical Colleges: Physician Supply and Demand through 2025: Key Findings (Internet); cited 2016 June. Available from: www.aamc.org/download/426260/data/physiciansupplyanddemandthrough2025keyfindings.pdf

30. Kerfoot, K: The Impact of Overtime on Employee and Patient Satisfaction (Internet) 2016 August 25, cited 2016 September. Available from:www.apihealthcare.com

31. Siemens Financial Services: Taking the Pulse: How Healthcare CFOs Around the World Are Managing Change [Internet] 2016; cited 2016 June. Available from: http://finance.siemens.com/financialservices/global/de/presse/studien/pages/whitepaper_2016_taking-the-pulse.aspx

32. Siemens Financial Services: Taking the Pulse: How Healthcare CFOs Around the World Are Managing Change [Internet] 2016; cited 2016 June. Available from:http://finance.siemens.com/financialservices/global/de/presse/studien/pages/whitepaper_2016_taking-the-pulse.aspx